Tax audits within criminal proceeding in 2017

Statistics. Turning point in court practice. Comments

Since autumn 2016 legal community actively raised the topic of illegality of delivery by investigating judges of decisions on the appointment of unscheduled tax audits within criminal proceedings (the first analytical material on this topic: “Tax audits within criminal proceedings: unlawfulness, inadmissibility, consequences“).

Now a year has passed from the moment when this topic became popular. What happenned with the court practice?

І.

As it can be seen from the analysis of court decisions available in the Unified State Register of Court Decisions (hereinafter – the “USRCD”), the investigating judges started to perceive positively the legal position on unlawfulness of appointment of such audits in many cases. Thus, for example, in the Court ruling of the Shevchenkivsky District Court as of October 26, 2017 in the case No. 761/38196/17 it is stated that:

That is the investigating judges increasingly deny such kind of petitions due to the lack of rights of both the prosecutors/investigators to apply with petition on appointment of tax audits within criminal proceedings and investigating judges to consider such kind of petitions.

ІІ.

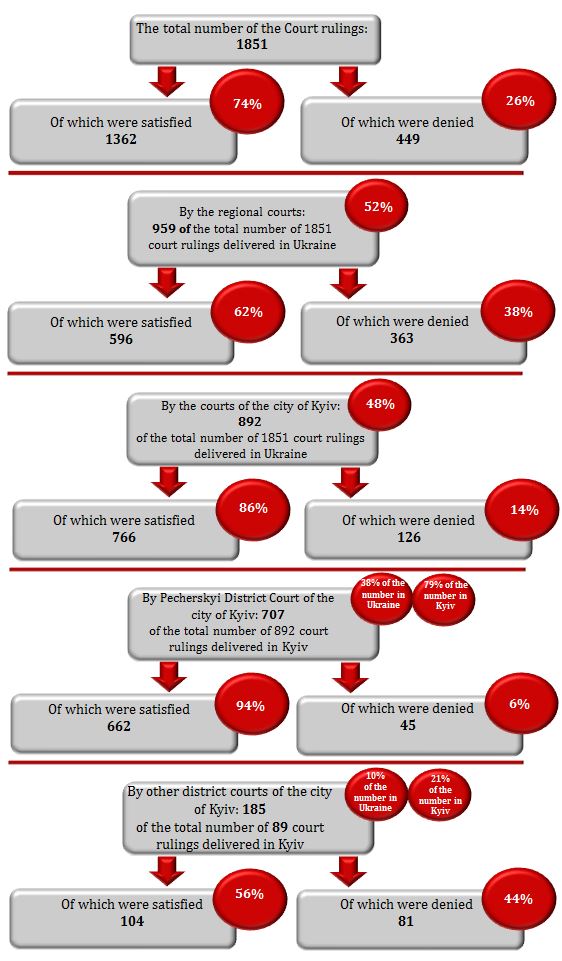

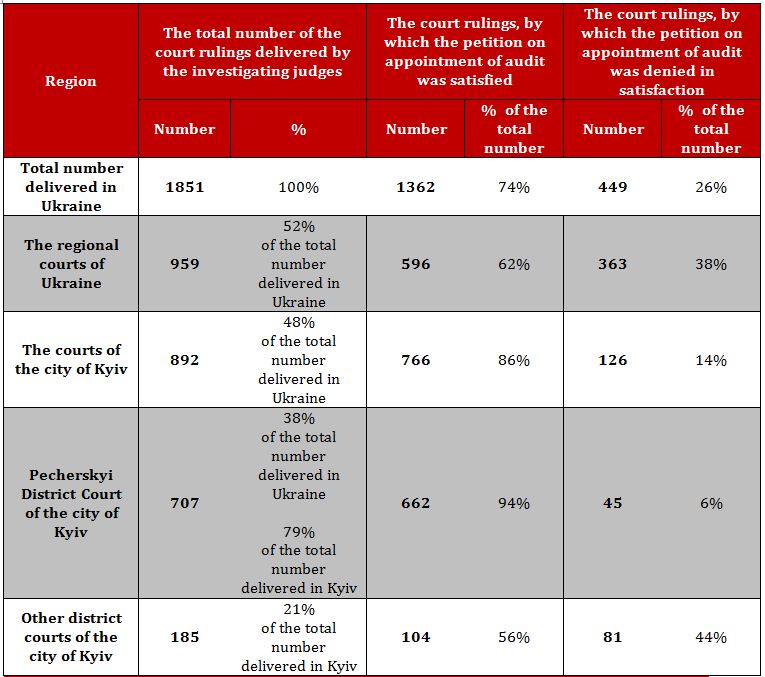

Within 9 months of 2017, according to the USRCD data, the investigating judges reviewed 1851 petitions of investigators/prosecutors on appointment of tax audit within criminal proceedings, of which:

So, it can be seen, that the District Courts of the city of Kyiv (without taking into account the data regarding the Pecherskyi District Court of the city of Kyiv) have better balance in the practice of delivering decisions by the investigating judges upon the results of consideration of petitions of investigators/prosecutors on appointment of tax audit. In such courts the practice of denial in satisfaction of petitions on appointment of tax audit has already reached the rate of almost 50 %.

The same situation can be seen in the courts of other regions of Ukraine, except for the city of Kyiv. The share of court rulings by which the investigating judges have satisfied and respectively denied in satisfaction of this kind of petitions of investigators/prosecutors on appointment of tax audit is more like the general situation in Ukraine.

Only Pecherskyi District Court of the city of Kyiv distinguishes itself with the sharp «turnabout» in the ratio of court rulings on appointment to denial in appointment of tax audit, having delivered 15 (!!!) times more court rulings on appointment of tax audit than on denial in its appointment.

In general, within Ukraine given the practice of denials of investigating judges in satisfaction of investigators/prosecutors’ petitions on appointment of tax audit within criminal proceedings, for taxpayers there is approximately one out of four chances that the investigating judge will deny in such a petition. Only a year ago, the number of denials in satisfaction of investigators/prosecutors’ petitions was almost close to zero.

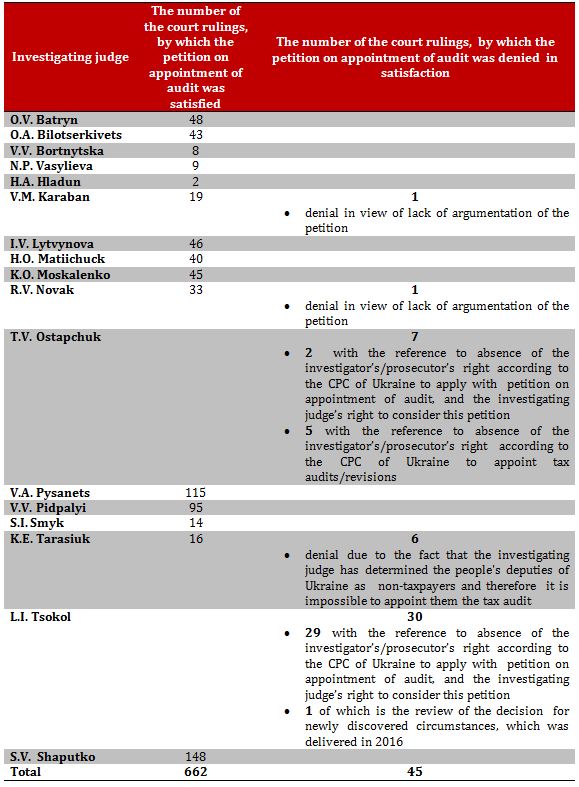

Herewith, for example, there are interesting facts about the Pecherskyi District Court of of the city of Kyiv:

That is the investigating judges within the same court are delivering diametrically opposite decisions. It’s interesting that the number of court rulings delivered by some judges who solely satisfy the petitions of prosecutors/investigators on appointment of tax audits within criminal proceedings greatly exceeds the number of court rulings by which other individual investigating judges deny in appointment of such audits.

Thus, for example, while the judge Shaputko Svitlana Volodymyrivna delivered 148 court rulings on appointment of tax audit within 9 month of 2017 (it is almost 1 such court ruling per day during 185 working days), another judge –Tsokol Larysa Ivanivna reviewed and resolved only 30 such petitions, having denied in appointment of tax audit. Similarly, while judge Pysanets Vitalii Anatoliiovych reviewed 115 petitions of investigators/prosecutors on appointment of tax audit, the judge Ostapchuk reviewed only 7 such petitions.

Such a variable statistic of the number of petitions of investigators/prosecutors on appointment of tax audit within criminal proceedings reviewed by investigating judges of the Pechersk District Court of the city of Kyiv raises questions regarding the fuctioning of the automatic case distribution system.

ІІІ.

At the same time, the appointment by an investigating judge of a court ruling on appointment of tax audit within criminal proceedings is not a “doom” yet, since the positive court practice of challenging such court decisions in the courts of appeal has formed.

So, inspite the fact that Article 309 of the Criminal Procedural Code of Ukraine (hereinafter – “the CPC of Ukraine”) does not provide any right to challenge court rulings on appointment of tax audit due to the fact that the CPC of Ukraine also does not provide any right to deliver such kinds of decisions – courts of appeal while admitting court rulings for review are guided by the Constitution of Ukraine, the general principles of the CPC of Ukraine and the practice of the European Court of Human Rights (hereinafter – “the ECHR”), in particular:

The Kyiv Court of Appeal by the new Court Ruling as of September 21, 2017 in the case No. 757/32144/17-k has cancelled the Court ruling of investigating judge on appointment of tax audit within criminal proceeding, stating that (quote):

“The challenged court ruling of investigating judge does not correspond with such requirements. Thus, Article 78 of the Tax Code of Ukraine provides that documentary unscheduled audit is carried out in the presence of at least one of the following circumstances: subpara. 78.1.11 of the Tax Code of Ukraine – court decision (of the investigating judge) on appointment of audit or resolution of authority that provides the operational detective work, investigator, prosecutor, adopted in accordance with the law. In means that the abovementioned provision refers to the Law according to which the said court decision should be obtained, and according to part 1 of Article 4 of the CPC of Ukraine, criminal proceedings at the territory of Ukraine are carried out on the grounds and in the manner stipulated by the CPC of Ukraine, regardless of the place where the criminal offense was committed. In other words, the procedural order for conducting criminal proceedings is defined in particular by the CPC of Ukraine, and other Laws of Ukraine (except for the CPC of Ukraine) do not establish the procedure for conducting criminal proceedings (cases). Besides, part 1 of Article 93 of the CPC of Ukraine states that the collection of evidence is carried out by the parties to the criminal proceedings, the victim, the representative of the legal entity in respect of which the proceedings are being conducted, in accordance with the procedure provided by the CPC of Ukraine.Furthermore it should be noted, that in accordance with the legal position set out in the Decision of the ECHR “Mikhailiuk and Petrov v. Ukraine” as of December 10, 2009 (para. 25 of the Decision), it is stated that the expression “in accordance with the law” requires firstly that the impugned interference has some basis in domestic law; it also refers to the quality of the law in question, requiring that it should be accessible to the person concerned, who must moreover be able to foresee its consequences for him, and be compatible with the rule of law.

Taking into account the lack of legal grounds in the CPC of Ukraine, the consideration of these petitions by the investigating judge is not covered by his powers, which must be implemented in the manner stipulated by the procedural law. In its turn, this prosecutor’s petition for appointment of documentary unscheduled audit of tax legislation requirements refers neither to the measures of ensuring the criminal proceedings within the meaning of Article 131 of the CPC of Ukraine, nor to investigative actions within the meaning of articles of Chapter 20 of the CPC of Ukraine, nor to covert investigative actions within the meaning of articles of Chapter 21 of the CPC of Ukraine, which have an exhaustive list, and consequently the CPC of Ukraine does not provide the right of investigator, prosecutor to apply to the investigating judge with petition on appointment of unscheduled documentary audit“.

The Odessa Region Court of Appeal by the Court ruling as of August 29, 2017 in the case No. 11-cc/785/1405/17 cancelled the court ruling of the investigating judge on appointment of tax audit within criminal proceedings stating that (quote):

“Thus, the Higher Specialized Court for Civil and Criminal cases in its letter No. 9-3139/0/4-16 as of December 27, 2016 confirmed the existence of a collision and indicated that it should be eliminated by the exclusion of subpara. 78.1.11 para 78.1 of Art. 78 of the Tax Code of Ukraine.

Letter No.04-18/11-60(10039) of the VRU Committee of INDIVIDUAL_5 on Legislative Support of Law Enforcement as of January 16, 2017 stated : “In court practice when dealing with the above issues in the criminal proceedings first of all one should be guided by the provisions of the CPC of Ukraine which under Article 1 of the Code are determinative in the assessment of the investigator’s actions. The order of the criminal proceedings, including procedural actions, is determined only by the Criminal Procedural Law of Ukraine”.

Thereby, the established by the court of appeal fact that the investigator’s petition does not comply with the requirements of the law, in particular the effective CPC of Ukraine does not contain the provision allowing the investigator to apply with this petition, groundless acceptance of this petition to consideration by the investigating judge and its consideration on the merits, which is not regulated by the effective CPC of Ukraine, according to opinion of the court of appeal makes the consideration of the investigator’s petition on the merits impossible, including consideration in the appeal instance. Hence, guided by provisions of Article 2.7, part 6 of Article 9 of the CPC of Ukraine the court of appeal considers it necessary to cancel the court ruling of the investigating judge as unlawful and groundless, and to close the proceedings in the case regarding consideration of the petition and return the petition to the pre-trial investigation body”.

The similar position is set out in the Court ruling of the Odessa Region Court of Appeal, which is available in USRCD by the link: https://reyestr.court.gov.ua/Review/53391774; http://reyestr.court.gov.ua/Review/68098926; http://reyestr.court.gov.ua/Review/68131687; http://reyestr.court.gov.ua/Review/69088090; http://reyestr.court.gov.ua/Review/69088710.

The Sumy Region Court of Appeal in the Court ruling as of August 16, 2017 in the case No.11-cc/788/355/17 cancelled the court ruling of the investigating judge on appointment of tax audit within criminal proceedings, stating that (quote):

“In the case «Steel and others v. the United Kingdom as of September 23, 1998 (para.54) the ECHR emphasized that «the Convention requires that all law, whether written or unwritten, be sufficiently precise to allow the citizen – if need be, with appropriate advice – to foresee, to a degree that is reasonable in the circumstances, the consequences which a given action may entail. The expressions “lawful” and “in accordance with a procedure prescribed by law” stipulate full compliance with the procedural and substantive rules of national law.

The ECHR in its other decisions also repeatedly pointed out to the imperfection of the effective legislation of Ukraine and to the necessity to comply with the legal certainty principle, in particular, in para. 31 of the case «Rakevich v. Russia», para. 109 of the case «Metropolitan Church of Bessarabia and Others v. Moldova», para 53 of the case «Yeloyev v. Ukraine» and para. 19 of the case «Novik v. Ukraine“.

Having regard to the system analysis of the abovementioned criminal procedural legislation of Ukraine, which does not refer the consideration of petition on appointment of tax audits to the competence of the investigating judge, taking into account the legal certainty principle, which is an integral and organic component of the rule of law, and which is settled in the practice of the Constitutional Court of Ukraine and the decisions of the European Court of Human Rights, the panel of judges chamber comes to the conclusion that the investigating judge does not have any legal and reasonable grounds to adopt a decision on conducting unscheduled documentary audit within criminal proceedings, since when considering certain petition of the pre-trial investigation body within criminal proceedings the executor of law, which in this context is the investigating judge of the court of first instance, should act in strict accordance with the law provision he has applied, within his competence, strictly comply with the procedure for considering petitions of investigators (prosecutors), in other words to comply with the principle of legality, according to which «it is allowed only to take actions stipulated by the law …

Thus, since the effective CPC of Ukraine does not provide the investigator with the right to apply to the court with such a petition, the same criminal procedural law does not establish the procedure for consideration of such petitions by the investigating judge, the panel of judges assume that they should not be considered in court at all, and the investigating judge when obtaining such a petition should deny in opening the proceedings.

In view of the above, the investigating judge, having considered on the merits the abovementioned petition of the investigator regarding unscheduled documentary audit, acted not on the basis of, not within the limits of her authorities and not in the manner determined by the law, and exceeded her discretionary authorities, which resulted into substantial violation of the criminal procedural law requirements”.

The Zaporizhzhya Region Court of Appeal in the Court ruling as of October 19, 2017 in the case No.1-cc/778/1160/17 cancelled the court ruling of the investigating judge on appointment of tax audit within criminal proceedings, stating that (quote):

“According to the requirements of part 3 of Article 26 of the CPC of Ukraine, the investigating judge, the court in the criminal proceedings deals only with that issues that are proposed for their consideration by the parties and assigned to their authorities by this Code (the CPC of Ukraine). In other words, taking into account the scope of the dispositivity principle , the procedural law clearly indicates the way the court and the investigating judge deal with the issue. Thus, the investigating judge should settle issues that are assigned to his authorities by the procedural law and in the manner stipulated by the procedural provisions.

Instead, when satisfying the investigator’s petition on appointment of unscheduled documentary audit of “Himex Limited” LLC on compliance with the tax legislation during the sale and purchase of shares in Private Joint Stock Company «Kremenchug Carbon Black Plant» in the absence of the procedural way of considering and dealing with these petitions, the investigating judge noted , that the court ruling is not subject to further challenge in the court of appeal.

Taking into account the legal position of the Constitutional Court of Ukraine expressed in the decision No. 3-рп/2015 as of April 8, 2015 (para. 2.1 of the decision), that according to the practice of the European Court of Human Rights the Article 6 of the Convention, which provides the right to a fair trial, does not determine the requirement for the state to establish court of appeal and cassation. However, the guarantees from the abovementioned article should also correspond with ensuring the effective access to the courts in places where such courts exist (para. 25 of the ECHR Decision in case «Delkour v. Belgium» as of October 17, 1997, para. 65 of the ECHR Decision in case “Hoffman v. Germany”, as of October 11, 2001 and para. 122 of the ECHR Decision in case «Kudla v. Poland» as of October 26, 2000).

Thus, the deprivation under certian circumstances of right of representatives of «Himex Limited» LLC to challenge the court ruling of the investigating judge would be a violation of the equality principles of every person all before the law and the court and access to justice.

Therefore, the panel of judges assumes that the appeal complaint submitted is subject to consideration.When considering the challenged court ruling, the panel of judges proceeds from the fact that in accordance with the requirements of Article 370 of the CPC of Ukraine, a court decision should be lawful, substantiated and motivated.

….

In the opinion of the panel of judges the challenged court decision, does not meet these requirements, since dealing with mentioned petitions is not covered by the the investigating judge’s authorities, which must be implemented in the manner provided by the procedural law, given that they concern neither measures of ensuring the criminal proceedingss, nor the investigative actions, nor to covert investigative actions.

Besides, the criminal procedural law of Ukraine does not provide the right of the investigator, prosecutor to apply to the investigating judge with petition on appointment of unscheduled documentary audit, moreover, the Criminal Procedural Code of Ukraine does not foresee any procedure for consideration of such petitions as well.

Whereas the investigating judge did not pay attention to the abovementioned, the challenged court ruling of the investigating judge is subject to cancellation, with the adoption of the new court ruling on denial in satisfaction of the abovementioned petition“.

Therefor, the abovementioned decisions of the courts of appeal, which canceled the court rulings on appointment of tax audits within criminal proceedings, confirm:

- the existence of the right to challenge such court rulings in the court of appeal;

- the unlawfulness of consideration of petitions of pre-trial investigation bodies and the adoption of court rulings on appointment of tax audits within criminal proceedings.

Accordingly, in general the legal position regarding the unlawfulness of adoption of court rulings on appointment of tax audit by the investigating judges is deemed positively by the courts.

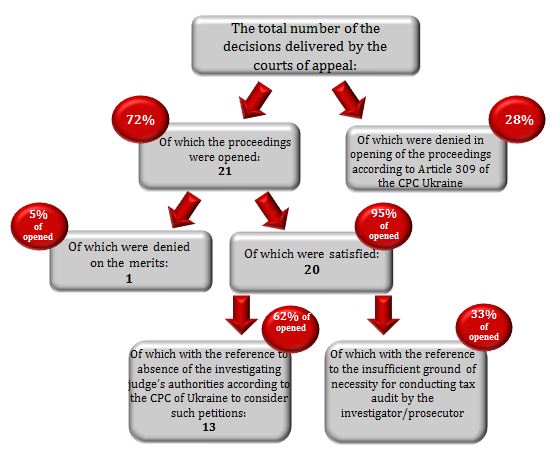

Thus, according to the monitoring of the data available in the USRCD, within 9 months of 2017 the courts of appeal delivered 29 court decisions upon the results of consideration of appeal claims on the court rulings of the investigating judges on appointment of tax audit within criminal proceedings.

Сonsequently, in 95 % of cases one can assert that if the court opens the appeal proceedings under the company’s claim on the court ruling of the investigating judge on appointment of tax audit, such challenge will be successful.

It should be noted, that most of denials in opening of the proceedings are unmotivated. Thus, for example, in the Court ruling of the Kyiv Court of Appeal as of August 31, 2017 in case No. 752/21365/16- к the Court stated:

Please be reminded that the court decision should be motivated. In denials of this kind we see the violation of Article 6 of the Convention on Human Rights and Fundamental Freedoms, as well as Article 129 of the Constitution of Ukraine.

It should be noted, that the problem of motivatedness of Ukrainian courts’ decisions is currently under the vigilance close scrutiny of the European Court of Human Rights (hereinafter –the “ECHR”), the practice of which is applied in Ukraine as a legal source in view of Article 17 of the Law of Ukraine «On execution of decisions and application of the European Court of Human Rights practice».

Thus, in particular, the Higher Administrative Court of Ukraine (hereinafter – “the HACU”) in its infoletter as of October 24, 2017, No. 1426/09-14/17, referring to the letter of the Government Commissioner for European Court of Human Rights, reminded the courts of lower instances about the necessity of making the court decisions motivated (see the newsletter by link).

Moreover, recently the Supreme Court of Ukraine in the Resolution as of December 10, 2017 in case No. 5-142кс(15)17, which is obligatory for the courts according to part 1 of Article 458 of the CPC of Ukraine, came to the following conclusions:

“In the case of adoption the court ruling by the investigating judge, that is not provided by the criminal procedural provisions, which the provisions of part 3 of Article 309 of the CPC of Ukrainerefer to, the court of appeal has no right to deny in review of its legality, giving reference to the provisions of part four of Article 399 of the CPC of Ukraine.

The right to challenge such court decision in the court of appeal is subject to be protected under paragraph 17 of the part one of Article 7 and part one of Article 24 of the CPC of Ukraine, which guarantee this right, taking into account provision of part 6 of Article 9 of the CPC of Ukraine, which stipulate that in cases when the provisions of the CPC of Ukraine do not regulate or ambiguously regulate the issue of criminal proceedings, the general principles of criminal proceedings defined by the part one of Article 7 of the CPC Ukraine are to be applied”.

Therefore, in accordance with the legal position of the Supreme Court of Ukraine , even if the investigating judge adopts a court ruling which is not subject to be challenged in accordance with Article 309 of the CPC of Ukraine, and which is not foreseen by the CPC of Ukraine, the court of appeal has the right to review it and, if there are reasons – to cancel.

Although this decision was delivered by the Supreme Court of Ukraine upon results of consideration of the prosecutor’s application and regarding another type ofthe court ruling, such a conclusion gives the unconditional right to review the court ruling of the investigating judge on appointment of tax audit within criminal proceedings in the court of appeal.

As results

Positive court practice has already gained a critical mass. We hope that the positive practice of the courts of appeal will begin to spread in geometric progression, and the unlawfull decisions of the investigating judges will be canceled, that eventually will lead to denial in consideration and satisfaction of petitions on appointment of tax audits within the criminal proceedings by the investigating judges.

However, this problem requires the final solution. Therefore, we expect that the problem of unlawfulness of delivering of the court rulings on appointment of tax audit by the investigating judges will be finally resolved by:

- either formation of the unified position of all investigative courts,

- or formation of the position on this issue by the new composition of the Supreme Court composition,

- or amending legislation,

- or formation of the ECHR practice on this issue.

We hope that this problem will be finally resolved as soon as possible by the final change in the practice of the investigating judges without «washing dirty linen in public», in particular beforethe ECHR’s eyes.

The above commentary presents the general statement for information purposes only and as such may not be practically used in specific cases without professional advice.

Kind regards,

SIMILAR POSTS

Criminal proceedings on tax evasion upon results of tax audit and dispute when the tax liabilities remain NOT settled ![]() 2857

2857

Alexander Minin and Ivan Shynkarenko spoke at the АНК Ukraine event “Tax audits of businesses: How to prepare and what to expect” ![]() 584

584

Statute of limitations: Restrictions for tax audits, application of sanctions, tax documents retention, and the impact of COVID/martial law ![]() 1887

1887

Tax audits: Types, criteria, and grounds for initiation ![]() 806

806

Renewal of tax audits: what shall be considered before deciding on allowing the tax authority to conduct the tax audit and during the tax audit? ![]() 1005

1005

Alexander Minin and Ivan Shynkarenko participated in the round table discussion “Tax and Customs Audits – Practice and Innovations” at AНK Ukraine ![]() 2150

2150

Is it impossible to challenge the tax audit orders even if they are issued in the absence of legal grounds? Should the taxpayer bite the bullet and tolerate the tax audit? ![]() 3600

3600

Scheduled documentary tax audit in 2024 appointed with the reference to low (compared to industry average) level of tax payment is illegal! ![]() 1860

1860

The “false bottom” of the Draft Law on communication between business and tax authorities No. 9662 ![]() 1245

1245

Yuliia Kryvomaz spoke at the online event of the Ukrainian Bar Association dedicated to recent court practice in tax dispute resolution ![]() 1024

1024

Leave a comment

Leave a comment